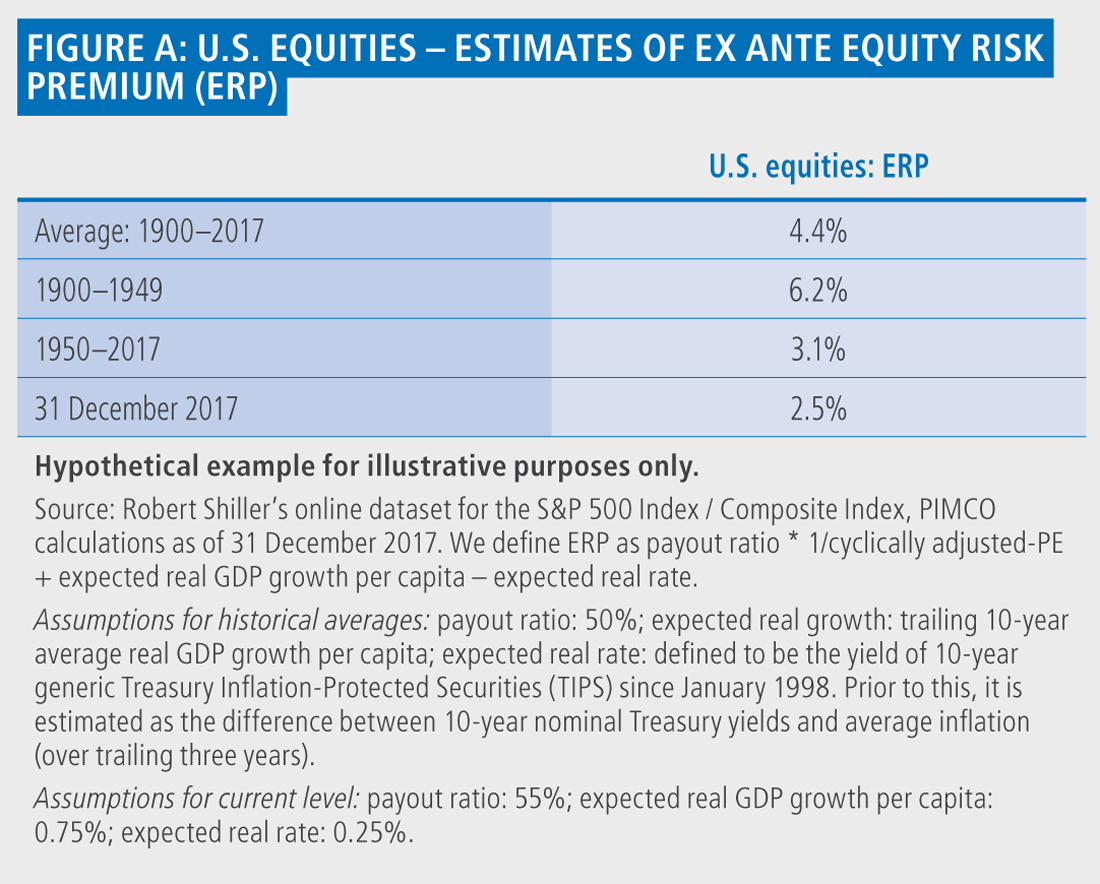

It is important to note that macroeconomic equity risk premium models are only appropriate for developed countries. Average market risk premium in the US.

Sep 10 2019 The average market risk premium in the United States rose to 56 percent in 2019 up 02 percentage points from the previous year.

Market risk premium ibbotson. 3232018 Small Cap Premium according to Ibbotson. -RXD 255 -RXY 432. Bond horizon premium Bills Real risk-free rate Real risk-free rate Real risk-free rate Inflation Inflation Inflation Source.

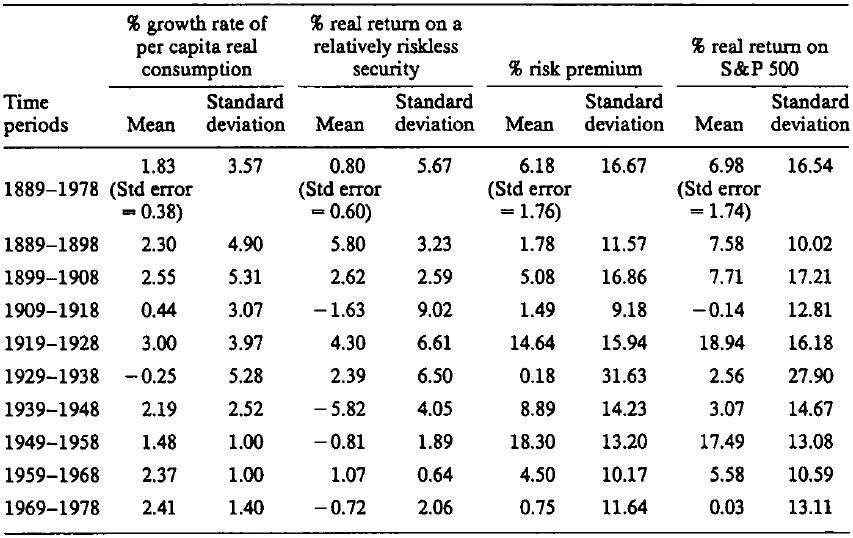

12162018 In Ibbotson and Chens supply-side equity risk premium model equity returns are composed from supply-side variables that describe the aggregate equity market. Market risk premium of 60 percent supply side Historical equity risk premium minus the PE ratio calculated using the 3 year average returns Small company premium Contingent on size of company Size decile based on market capitalization Size premium. Benchmark against which to measure risk premiums.

An IRP of zero implies that the industry has the same risk as the market. William Goetzmann and Roger Ibbotson are two leading researchers on the equity risk premium whose empirical work has invaluably enriched the literature. The Equity Risk Premium University of Texas at Austin.

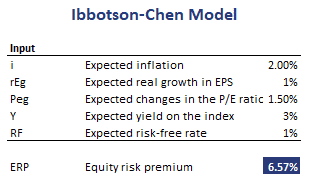

The 10-year German government bond yield was 128 as of end-of-March 2013 resulting in an implied equity risk premium of 786. The Ibbotson-Chen model is a macroeconomic model for the Equity Risk Premium ERP. Low-cap companiers USD 202m-USD 773m.

To estimating the risk premium Real Equity Risk Premium can then be estimated by subtracting short-term commercial paper yields from RD and RY which leaves RXD and RXY respectively Main Result. 2011-2019 Statista. G12 G31 M21 Keywords.

1312019 Roger Ibbotson and James Harrington discuss two different ways of measuring the relative performance of small stocks versus large stocks in this article. Note that the first three terms inflation real risk-free rate and bond horizon premium are typically combined into the long-term yield of a riskless bond because this yield. Ibbotson developed an industry premium methodology that appraisers can now reference and cite in their appraisal reports.

This return compensates investors for taking on the higher risk of. Wiley 2016 Valuation Handbook Guide to Cost of Capital. Equity premium required equity premium expected equity premium historical equity premium.

This suggests that investors demand a slightly higher return for investments in that country in exchange for. 1302013 To add to the data Jorion and Goetzmann 1999 estimated a geometric Equity Risk Premium of 283 for the period pre-dating Ibbotsons figures 1792 to 1925 and based on thirty-nine countries. An IRP greater than zero implies that the industry is more risky than the market.

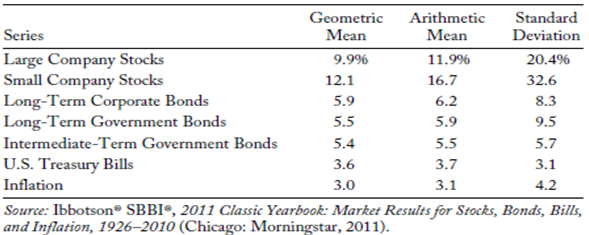

Morningstar U S Ibbotson Associates Published Research. Based on the risk premium data from Ibbotson Associates previously discussed the cost of equity or the discount rate with no specific company risk premium is 21 which results in a capitalization multiple of 48. For the 78 years 1926 through 2003 the risk premium for large stocks over.

6 The most common reference for MRP in the US is from Ibbotson Associates and the most common period is from 1926. Professors analysts and companies that cite Ibbotson as their reference use MRP for the United States between 2 and 145 and the ones that cite Damodaran as their reference use MRP between 2 and 108. 1292020 The average market risk premium in the United States remained at 56 percent in 2020.

Ibbotson Equity Risk Premium Still Out There Canadian. Large companies USD 3322m. These supply factors include inflation earnings the PE ratio and dividends.

An equity risk premium is an excess return earned by an investor when they invest in the stock market over a risk-free rate. To equity of 100000 per year in perpetuity with zero growth. Using data from the period 1951 to 2000 for the US market ie SP 500 they find that.

Ibbotson and Harrington demonstrate why using a non-beta-adjusted size premium within the context of the capital asset pricing model CAPM to estimate cost of equity capital will likely double count beta risk and therefore overstate risk. This book of essays pulls together their research on the topic which has spanned decades. Macroeconomic models are based on the relationship between macroeconomic variables and financial variables.

Mid-cap companies USD 774m-USD 3321m. Investors who are more skeptical might also want to apply the most pessimistic dividend and earnings forecast across all analysts. I the small stock premium and ii the beta-adjusted size premium.

5252012 Ibbotson - ERP Data from Ibbotson Associates Stocks Bonds Bills and Inflation 2011 Yearbook published by Morningstar. Based on this the company is valued at roughly 476000. US MARKET RISK PREMIUM USED IN 2011 BY PROFESSORS.

The equity market risk premium MRPis the average return that investors require over therisk-free for accepting higher variability in returns that are common forequity investments i e the MRP reflects a minimum threshold. Ibbotson 2011 Ibbotson and Siegel 1988.

Https Faculty Mccombs Utexas Edu Keith Brown Afpmaterial Topicc10 1 Pdf

-

Cari produk Economy Book Import lainnya di Tokopedia. Here are solid guidelines on when and what to buy sound reasons for selling common st...

-

A USA company hiring even more workers now. Find the latest FuelCell Energy Inc. First Week Of October 15th Options Trading For Fuelcell ...

Featured Post

trivia for today in history

100 History Trivia Question With Answers Reader's Digest . Web U.S. history trivia Question: When was the Declaration of Independ...